In any undergraduate class, when introducing derivatives, you can be sure that the first two being mentioned will be forwards and then futures. One exchanged over the counter, the other one traded in exchanges. One "tailor-made", the other one highly standardized. The first one exposes parties to counterparty default risk, the second one eliminates this risk through the Clearing House's intervention. However, having the same payoff structure, one might think that also the pricing mechanism would be identical. At this point, one feature which characterizes futures must be interpelled: the Marking to Market mechanism. Namely, the CH adjusts each party's margin account every day based on the price performance of the underlying asset. This important feature has got a subtle but significant impact on pricing these contracts when the underlying is interest rate-related. Derivative contracts written on interest rates represent the largest category; one thing which needs to be precised is that when a forward is written on a certain interest rate, it is referred to as Forward Rate Agreement (FRA).

The Marking to Market (MTM) process allows parties in a future to immediately reinvest potential profits coming from daily oscillations of the underlying asset thanks to their account being adjusted at the end of every trading day. Now, if the underlying is positively correlated with interest rate movements, the MTM creates a double benefit for the long position: not only the margin account will rise at the end of the day, but also the proceeds will be potentially reinvested at a (marginally) higher rate. On the other hand, if the asset is negatively correlated with basis point variations, such as traditional floating rate bonds or Eurodollar futures, the MTM reveals to be a double-edged sword for long positions: the underlying's price loses ground and what can be reinvested at a risk-free rate will yield out (marginally) lower returns. The only case in which futures' prices are assimilable to forwards' ones consists of contracts whose underlying is totally uncorrelated with rates.

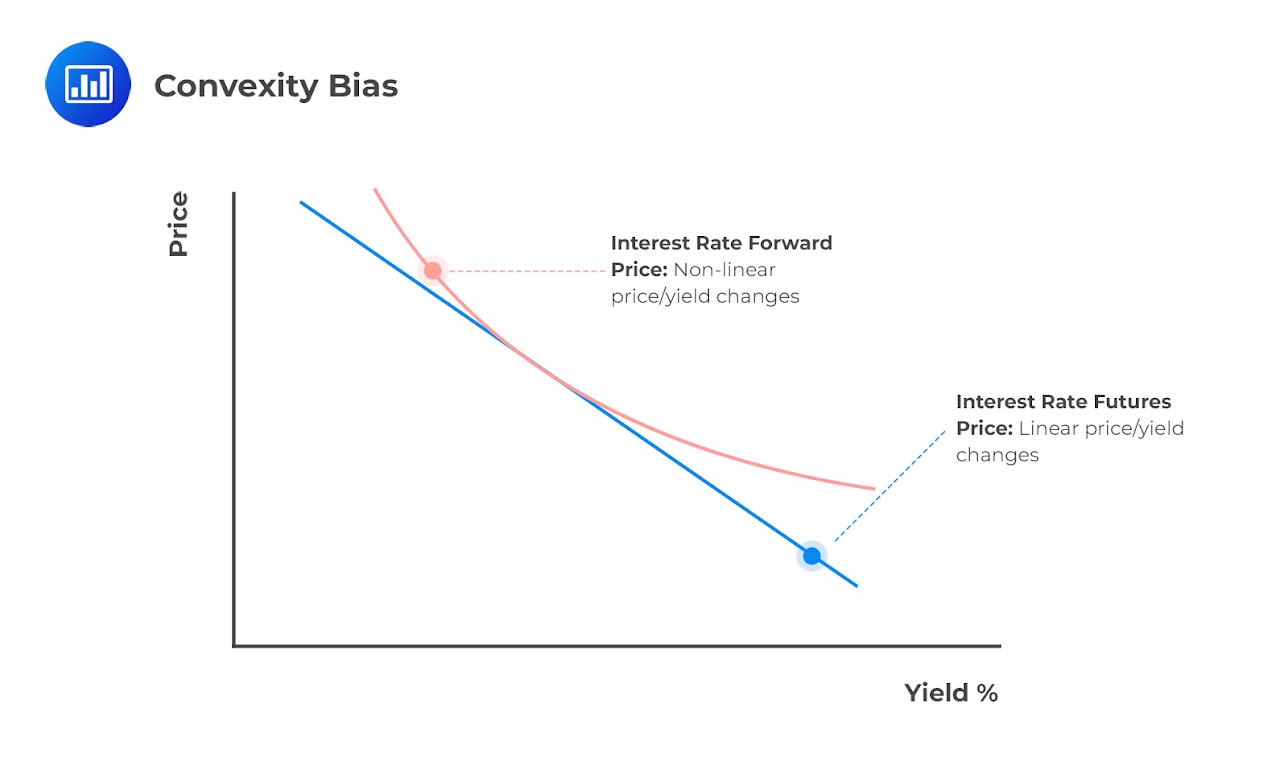

Speaking mathematically, while the price of a future in function of the underlying's interest rate has got a linear relation with bp changes, influenced by the MTM mechanism; the price of a FRA is connected to rate changes through a non-linear relation, more precisely a convex one. This is why the adjustment needed for forward prices to eliminate the effect of the MTM is called convexity bias.

The deterministic adjustment for the bias is gifted us by the beautiful Ho-Lee model, a stochastic risk-neutral process for the instantaneous short rate, where increments are modelled as a Wiener process. While computations are quite advanced, involving Ito's lemma, the final formula is:

where:

σ = annualized volatility of the short rate;

T₁ = time to expiry;

T₂ = end of forward period.

From the price of a future written on an interest rate, the implied future rate itself is easily obtainable:

The implied future rate represents the expected spot rate at expiry date under risk-neutral expectations. What do we mean by "risk-neutral" ? It is just a convenient measure to price interest rate securities through much easier computations. In practice, the risk-neutral probability is the one which makes the market price of interest rate risk null. It does it by usually assigning a little more weight to rates being higher than actual expectations rather than being lower. Anyways, the incredibleness of this framework is that the assigned probabilities do not matter in pricing computations at the end, making the risk-neutral probability an extremely useful tool. The message is: expectations and actual probabilities are essential, for instance, for risk assessment, but not for pricing, where what really matters is that prices of related securities are consistent between them, making arbitrage impossible.

What we are missing to comprehend is the actual relation between these implied future rates and forward (FRA) rates. First, we need to specify that the price of a ZCB (i.e. Zero Coupon Bond) from T1 to T2 can be found through:

where:

P = price;

r = continuously compounded interest rate;

T-t = time to maturity.

We can compute today's price (T0 < T1) of a ZCB from T1 to T2 using both the discounted risk-neutral expected price at T1 and the discounted price based on the FRA rate. Both relations are decreasing convex functions and they must hold simultaneously, so we can pose them equal. By Jensen's inequality, the discounted risk-neutral expected price at T1 must be greater than the discounted price based on the expected risk-neutral rate. Therefore, the price based on the FRA rate must also be greater than the one which lays on the expected risk-neutral rate. Hence, being decreasing convex functions, the forward rate is always lower than the expected risk-neutral one, namely the implied future rate. The difference consists exactly of the convexity bias:

Source: AnalystPrep

For those interested in deepening and clarifying the aforementioned proof for which future rates are always greater than forward ones, here is the furtherly detailed mathematical explanation.

References

[1] John C. Hull. “Technical Note No. 1: Convexity Adjustments to Eurodollar Futures.” Options, Futures, and Other Derivatives. University of Toronto, Rotman School of Management, 2023.

[2] Pietro Veronesi. Fixed Income Securities: Valuation, Risk, and Risk Management. John Wiley & Sons, 1st edition, 2010.