Abstract

In recent years, the options market on the S&P 500 index had a structural transformation that, despite its profound implications, has received relatively limited attention in mainstream financial discourse. At the center of this change are the so-called zero days to expiration options (0DTE): option contracts that expire the same day they are traded. What until a few years ago was a small segment has now become the most active part of the entire U.S. derivatives market.

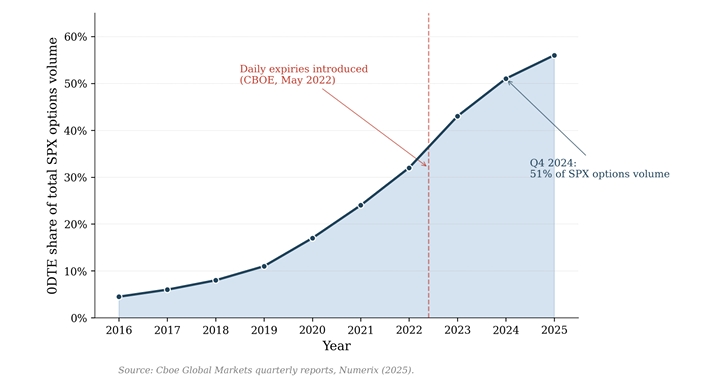

The numbers speak by themselves. In the fourth quarter of 2024, 0DTE options on the S&P 500 surpassed all other expiration dates combined in terms of volume. The growth, therefore, has not been gradual, it has been a structural break.

[Figure 1: Growth of 0DTE options as a share of total SPX options volume, 2016–2025. The dashed line marks the introduction of daily expiries by CBOE in May 2022, after which the segment accelerated from ~32% to over half of total volume in less than three years.]

The argument developed in the rest of this paper is that the structural impact of 0DTE options does not just lie in their volume, but in the mechanical hedging response they impose on dealers, and in the way this response reshapes the microstructure of the underlying market. As time to expiration collapses, the mathematics of delta hedging breaks down, and the resulting flows transform the futures market from an instrument for price discovery into a transmission channel for options positioning, with measurable consequences on intraday volatility, on the behavior of prices in the final hours of the trading session, and on the way market makers manage their residual risk.