Carry trade represents an extremely interesting macrofinancial dynamic as it often uncovers hidden capital flows which affect currencies from all around the globe, as enjoyable in "The Shadow Channel of Global Credit: How Carry Trade Moves Economies".

In particular, 2025 proved to be a surprisingly positive year for emerging markets and Forex carry, advantaged by low interest rates volatility and stability in the US Dollar and in general global trade, despite early year's catastrophic premises. Among EM carry trade targets, Brazil, Egypt, Nigeria and Columbia shone particularly brightly, recording over 20% returns year-to-date when funded out of the Dollar. As a natural consequence, many eyes and market indices are now closely following their performances.

But there is a story few ones are speaking about: the Ugandan Shilling delivered fine return, about 10%, throughout 2025, and might be ready to shine also in the upcoming times. Return was fairly shared among yield and real exchange rate appreciation, suggesting an inspiring balance. Nominal policy rate was maintained at 9.75% in November by the Bank of Uganda, forecasts indicate that cuts will reduce it until 8% in 2027, supporting a promising economic growth and riding the wave of a decreasing inflation rate, which hit a 7-months low of 3.4% in October.

A key word which is making the Ugandan Shilling such appealing to foreign investors is stability: nominal interest rates have been pretty stable in recent years, driven by credible central bank inflation targeting and developed local markets compared to peer countries. In the meanwhile, nominal exchange rates have showed some solid flexibility, with the Shilling appreciating by 13% since 2024.

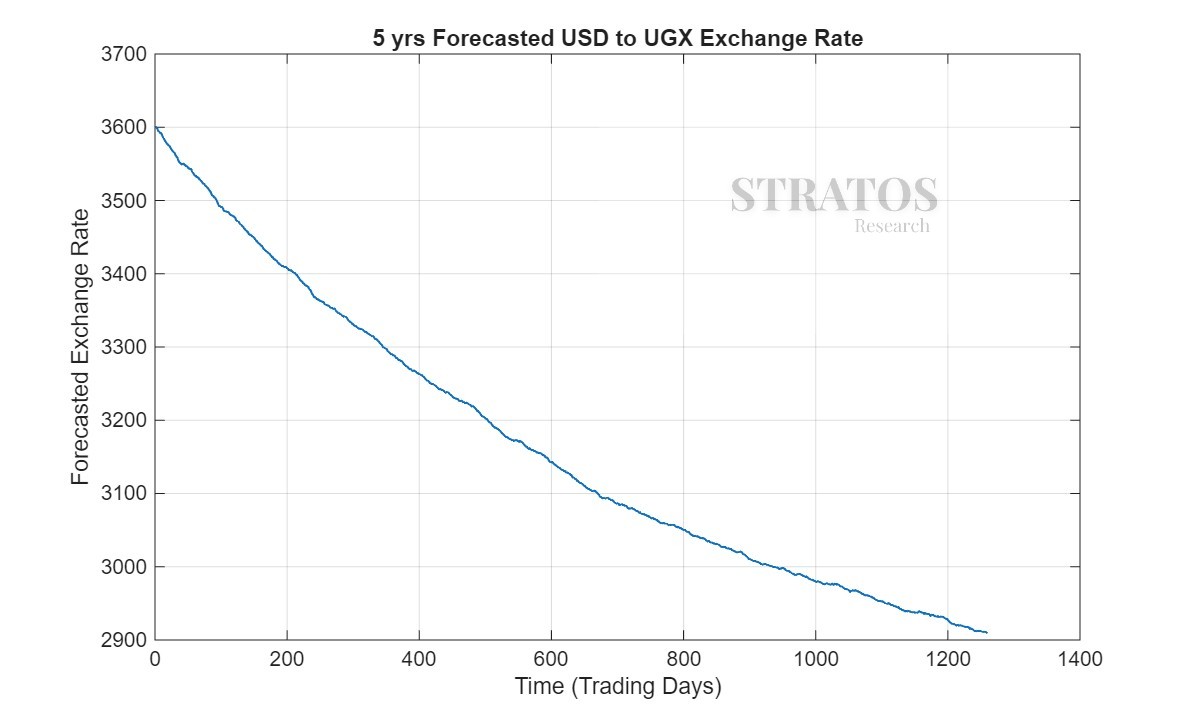

We forecasted the USD/UGX real exchange rate over the next 5 years, based on a mean-reversion model advised by an ECB research, with half-life level at 3 years and mean-reversion level represented by the sample average real exchange rate over the last 20 years, which not casually consists of with the rate driven by Purchasing Power Parity (PPP Rate).

While this model might not be the best one to capture short-term oscillations, its real strenght lies in the capability to predict the trend to a mid-long term equilibrium rate. In this case, it's showing a significant appreciation of the Shilling with respect to the Dollar in the upcoming 5 years.

Economic growth expected by investors will be mostly driven by oil sector development and increasing foreign direct investments, laying the groundwork to narrow the current account deficit. On the other side, worries about Uganda's situation include low foreign currencies reserves, making the country more exposed to exchange rate risk; a still limiting speculative credit rating (B- by Standard&Poors, but with positive outlook) which increases financing costs; finally possible political risks linked to elections occurring this January.

Overall, if these are the premises, the Ugandan Shilling could be the real next big diamond among EM carry trade targets. However, stability must continue to be a key word not only in terms of rates, but also in a geopolitical context which has often proven to be a powder keg ready to explode.